It is not how much you make, but how much you keep!

Tax planning is the analysis of a financial situation or plan from a tax perspective. The purpose of tax planning is to ensure tax efficiency. Through tax planning, all elements of the financial plan work together in the most tax-efficient manner possible. Tax planning is an essential part of a financial plan. Reduction of tax liability and maximizing the ability to contribute to retirement plans are crucial for success.

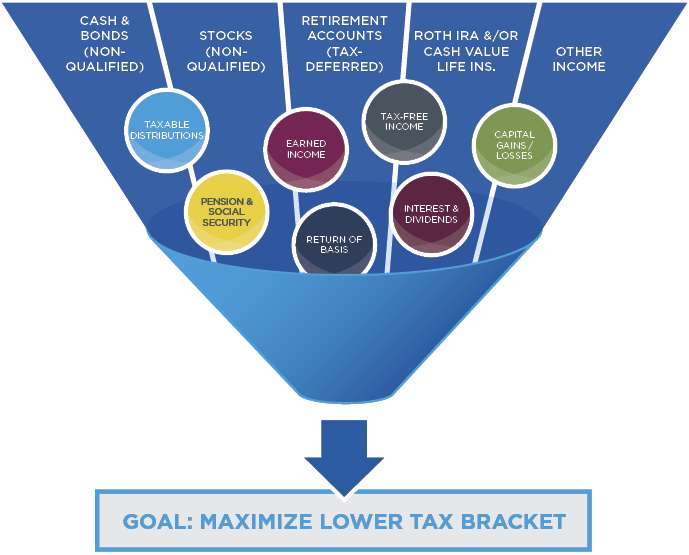

How Tax Planning Works

Tax planning covers several considerations. Considerations include timing of income, size, and timing of purchases, and planning for other expenditures. Also, the selection of investments and types of retirement plans must complement the tax filing status and deductions to create the best possible outcome.

- Tax planning is the analysis of finances from a tax perspective, with the purpose of ensuring maximum tax efficiency.

- Considerations of tax planning include timing of income, size, timing of purchases, and planning for expenditures.

- Tax planning strategies can include saving for retirement in an IRA or engaging in tax gain-loss harvesting.

Tax Planning for Retirement Plans

Saving via a retirement plan is a popular way to efficiently reduce taxes. Contributing money to a traditional IRA can minimize gross income up to $6,500. As of 2018, if meeting all qualifications, a filer under age 50 receives a reduction of $6,000 and a reduction of $7,000 if age 50 or older. For example, if a 52-year-old male with an annual income of $50,000 who made a $6,500 contribution to a traditional IRA has an adjusted gross income of $43,500, the $6,500 contribution would grow tax-deferred until retirement.

There are several other retirement plans that an individual may use to help reduce tax liability. 401(k) plans are popular with larger companies that have many employees. Participants in the plan can defer income from their paycheck directly into the company’s 401(k) plan. The greatest difference is that the contribution limit dollar amount is much higher than that of an IRA.

Long-term capital gains are taxed based on the tax bracket in which the taxpayer falls.

- 0% tax for taxpayers in the lowest marginal tax brackets of 10% and 15%

- 15% tax for those in the 25%, 28%, 33%, and 35% tax brackets

- 20% tax of those in the highest tax bracket of 39%

Up to $3,000 in capital losses may be used to offset ordinary income per tax year. Remaining capital losses can be carried over with no expiration to offset future capital gains.