Let us solve your life insurance puzzle!

Let Blue Chip Macro guide you in choosing the proper life insurance policy. Know the pros and cons of your choices will make you an informed consumer so you’ll be able to better understand the options you’re presented. Make the right choice for you and your family with confidence from an unbiased advisor instead of a life insurance agent who works on commission!

The different types of life insurance can be divided into term and permanent, depending on how long they are in effect. This most common permanent life insurance is whole life. Some types of life insurnace expire, some have an investment-like cash value, and some are best for older or unhealthy applicants. There are benefits and drawbacks to each.

Specific types of life insurance include:

- Term life insurance

- Permanent life insurance

- Whole life insurance

- Universal life insurance

- Variable life insurance

- Variable universal life insurance

- Simplified issue life insurance

- Guaranteed issue life insurance

- Final expense insurance

- Group life insurance

- What life insurance policy type is right for me?

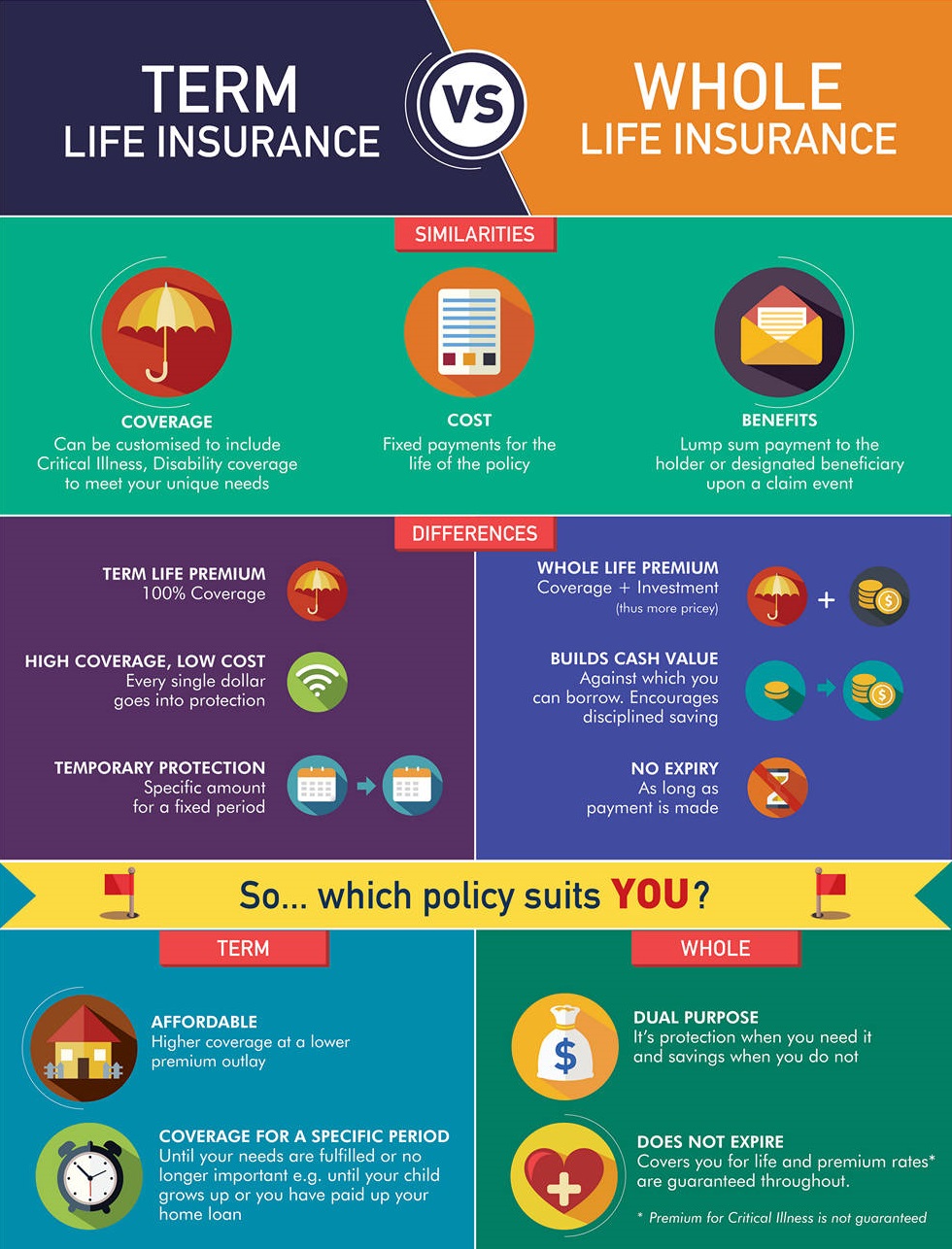

Term life vs whole life

The most common decision people make when it comes to life insurance is term versus whole.

Term life insurance is a "pure" insurance policy: when you pay your premium, you’re just paying for the death benefit that goes to your beneficiaries in the event of your death. The death benefit can be paid out as a lump sum, a monthly payment, or an annuity, although most people ask the insurance company for the lump sum.

Term policies are more affordable compared to their peers, costing between $30-40 a month for a 30-year, $500,000 policy for healthy people in their 20s and 30s. They expire at the end of the term, which lasts up to 30 years.

Whole life insurance, on the other hand, has a death benefit but also a cash value, where the premiums you pay monthly or annually are partially used to fund that cash value. A major part of the premium goes to fees and maintaining the death benefit; over time, the fees portion decreases and more of the premium goes directly to funding the cash value.

Due to the fees and the extra feature, a whole life insurance policy can cost six to 10 times as much as a term life policy (for the same death benefit amount).

Whole life lasts for as long as you pay the premiums. However, the cash value component can make whole life more complex than term life because you have to consider surrender fees, taxes, and interest as well as other stipulations.

Still, it may be worth it if you need the cash value to cover things like endowments or estate plans, which might benefit from the greater options that a whole life policy provides.

Permanent life insurance

Permanent life insurance is an umbrella term that covers several different, more specific life insurance types. In general, permanent life policies will last for as long as you pay the premiums, and they have a cash value component.

Whole life insurance is a type of permanent policy, so a lot of the same pros and cons we discussed above can apply to the other types.

Still, there are some key differences in the various types of permanent life insurance policies, so they’re worth talking about further.

Universal life insurance

Universal life insurance has a cash value, just like a whole policy. Your premiums go toward both the cash value and the death benefit.

But there’s a twist: the policyholders of universal life policies can change the premium and death benefit amounts without getting a new policy.

Basically, although you have a minimum premium to keep the policy in force, you can use the cash value to pay the premium. That means if you have enough money in the cash value, you can use that to skip premium payments entirely, letting the accrued interest do the work.

But the cash value of a universal life insurance policy has an interest rate that’s sensitive to current market interest rates. If the interest rate being credited to your policy decreases to the minimum rate, your premium would have to increase to offset the reduced cash value.

You can also adjust the death benefit within limits outlined in your policy. Increasing it may subject you to further underwriting, while there may be fees to decrease it.

If your financial situation changes, the ability to change the death benefit amount within your policy is appealing. While this can be done with term life insurance policies, this feature is one of the main selling points of a universal policy.

This flexibility makes universal life insurance attractive to some people, but it’s also confusing. Unlike term insurance, where you pay a certain amount every month or year and know what the death benefit will be, shifting premiums and death benefits are more complex than what most people need, and it comes at an added cost.

Variable life insurance

The main difference between variable life insurance and whole life insurance is how the cash value component works.

With a whole life insurance policy, the cash value component is a savings account. That’s why, although the growth might be small compared to other investment options, there is a guaranteed minimum rate. It also includes dividend payments from the life insurance company.

A variable life insurance cash value, though, is more along the lines of what you’d expect when you think of investing: a series of mutual fund-like sub-accounts where you can get some decent growth, but you can also lose money depending on the market. The cash value is more or less placed in the stock market.

While this makes variable life insurance policies a better investment option than whole life policies – the potential for higher, tax-deferred growth makes it a "super-IRA" – you can only invest in the sub-accounts available through your policy. That means you don’t get to choose from the wide variety mutual funds that are available on the open market.

While fees can be lower with a variable life insurance policy than a whole life policy, the product is riskier.

Why?

The same reason investing in stocks is risky: most people don’t know much about the stock market and don’t know enough to make changes in their investment. There’s too much management for the average person to do it effectively.

All of this makes a variable life insurance policy both a limited investment option and a limited life insurance option.

Variable universal life insurance

If you think variable universal life insurance is just some aspects of universal and variable life insurance policies mashed together…well, you’re mostly right.

A variable universal life insurance policy takes the best (or worst, depending on how you look at it) of the other two policies: you can adjust the premium and death benefit amount while investing the cash value in the policy’s sub-accounts.

But variable universal life insurance also comes with the same headaches as the other two. Again, this is more complicated than most people looking for life insurance need, and it isn’t your best available option for an investment or insurance.

The better option is a combination of a simple, cheaper term life insurance policy and a dedicated investment option, like a mutual fund. This offers the same insurance coverage as a variable universal life insurance policy with lower fees and easier administration.

Simplified issue life insurance

Typically when you apply for life insurance, you go through a paramedical exam as part of the underwriting process so the insurer can find out how risky you are to insure. Ultimately, it helps them set your premium rate.

With simplified issue life insurance, though, you can skip the medical exam. That’s the "simplified" part of this policy type: known as a "no exam policy", a simplified issue policy gets you life insurance without the health exam.

You’re not out of the woods completely, though. You don’t need to go through the medical exam, but you do need to fill out a health questionnaire, answering questions like if you smoke, have been diagnosed with serious illnesses, and so on.

People in poor health may have to take the exam if they have too many health issues, and they could flat-out be denied by insurers. For those healthier people in a hurry, though, it might be a good option to skip scheduling the paramedical exam, which adds some time to the underwriting process.

But with this benefit comes a major financial drawback.

With a term life insurance policy, your premium rates are directly tied to your chances of outliving your policy. If you’re young and/or healthy, you’ll pay lower rates than someone who is older and/or in poor health.

That’s why the medical exam is important. Since there is no medical exam with simplified issue life insurance, the policies tend to be more expensive than term policies.

Guaranteed issue life insurance

Guaranteed issue life insurance takes the concept of simplified issue life insurance – forgoing the health exam – and takes it a step further in that you don’t have to answer any questions about your health, either. As long as you can pay the premium, the insurer will cover you, needing only your age, sex, and state of residence.

That makes it appealing for older people, whose declining health makes it prohibitively expensive to get coverage with another insurance types.

Guaranteed issue life insurance is useful for elderly applicants, but others can likely get more life insurance coverage at a lower cost with a different policy type.

Just like with simplified issue life insurance, the lack of insight into your health conditions that a medical exam and interview would provide means that you’re going to be paying more for coverage. In order to cover the costs of an average funeral, you’d have to pay more than $200 a month for around $10,000 of coverage.

Final expense insurance

Still looking for a way to cover funeral costs if you passed on guaranteed issue life insurance? You’re in luck, because there’s a life insurance policy that’s specifically for that purpose.

Final expense insurance is a unique type of policy: it covers the cost of anything associated with your death, whether its medical costs, a funeral, or cremation – whatever your literal final expense is. It’s usually only issued to people of a certain age and the policy is valid up to a certain age.

Like permanent life insurance policies, there’s a cash value that can grow over time. Final expense insurance is a simplified issue policy in most cases, but if you don’t pass the health questionnaire you’ll be placed in a guaranteed issue policy instead.

Final expense insurance is usually attractive to older people who don’t have other life insurance coverage (maybe they outgrew their term life policy) and don’t have enough savings to pay for their own funeral, which can cost upwards of $8,000.

Coverage is usually for small amounts, from $5,000 to $25,000, to cover those expenses. It’s good if you don’t have another way to pay for your funeral and don’t want to burden your family with the costs.

However, it has the same drawbacks as guaranteed issue life insurance: higher life insurance premiums for relatively low coverage amount. If you or your family are able to pay for a funeral through other means, that’s your best bet.

Group life insurance

Group life insurance isn’t technically a life insurance type, but it’s important to know how it's different from privately purchased term life.

If you have life insurance provided through your employer, you’re familiar with group life insurance. Group life insurance is most commonly term (although it can be whole). The real reason we bring it up, though, is that most people think their employer life insurance is enough, when in most cases it isn’t.

Make no mistake: if your employer is offering life insurance at no extra cost to you, it’s a great benefit. By all means, get insured. But if you need life insurance to protect your family, employer-provided coverage may not be sufficient.

Employer life insurance provides fairly low coverage, usually only one to two years’ worth of salary, when you could need $500,000 or more in coverage in order to meet your financial obligations.

If you want to go for more, it’s likely to be more expensive than buying your own policy if you’re a person in relatively good health.

In short, don’t automatically pass up group life insurance, but don’t automatically dismiss other options, either. Make sure it fits your needs and see how you can work it into your private coverage.

Blue Chip Macro is an independent fee only Registered Investment Finanical Advisor that was founded in 2002 and is based in Santa Monica, California. We primarily serve the Los Angeles area and offer financial planning, business consulting, asset management, wealth managment, life insurance consulting and many other financial services. Our specialty is wealth and asset management through investing in stocks. Contact us for a FREE CONSULTATION to see how Blue Chip Macro can help you navigate the maze and find the life insurance that is best for you and your family!